| General Discussion Undecided where to post - do it here. |

| Reply to Thread New Thread |

10-04-2011, 11:53 PM

10-04-2011, 11:53 PM

|

#1 |

|

|

http://www.merkfunds.com/merk-perspe...011-10-04.html ...

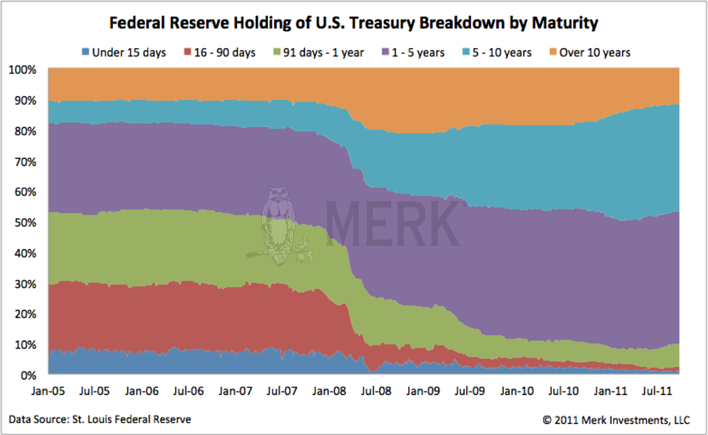

Axel Merk, Portfolio Manager, Merk Funds October 4, 2011 Is Operation Twist a failure? The stock market plunged in disappointment when it was announced. Keynesians are tearing their hair out in frustration, as it appears the Fed failed to ramp up the printing press. Free marketers are disgusted by the blatant manipulation of the yield curve. A number of Federal Reserve (Fed) President Bernanke’s colleagues dissented and/or are voicing public opposition. However, as the dust settles, it appears there is a method to the twist: Bernanke may have a plan…  To understand where we may be heading, let’s look at where we have come from. Below is a graphical depiction of the Federal Reserve’s holdings of Treasury securities on its balance sheet; the different colors represent the evolving composition of the maturity of assets held by the Fed: White Papers Merk White Papers provide in-depth information into currency as an asset class. Portfolio Benefits of The Currency Asset Class The Currency Asset Class: A New Era of Investment Opportunity The Archive: Merk White Papers  One does not need to be an economist to see that the Fed has already been “twisting” its holdings of Treasury securities. It used to be that over 50% of Treasuries held by the Fed had a maturity of less than a year. That portion has already shrunk dramatically. Operation Twist is going to focus on the purple shading, replacing many of these securities with longer-dated ones. Differently said, Operation Twist really is nothing new, but an extension and expansion of policies in place since 2008. |

|

|

10-04-2011, 11:54 PM

|

#2 |

|

|

2008.

Indeed, Bernanke has a playbook, hiding in plain sight: in his 2002 speech that earned Bernanke his nickname as “Helicopter Ben”, he laid out his plan when faced with the threat of deflation. Whereas his predecessor Paul Volcker took years to convince the markets that the Fed was serious about fighting inflation, Bernanke appears to be relentless in trying to convince the markets that deflation is not going to happen in his back yard. But why not simply print more money as the economy has slowed (engage in “QE3”)? It looks like Bernanke at least wants to maintain the appearance of keeping long-term inflation expectations low. Earlier this year, Bernanke complained a few times that the risk-reward ratio of another round of easing is not all that clear. Well, how about making it clearer, by:

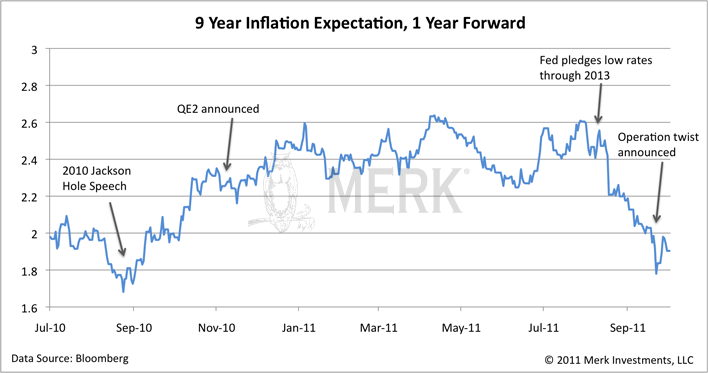

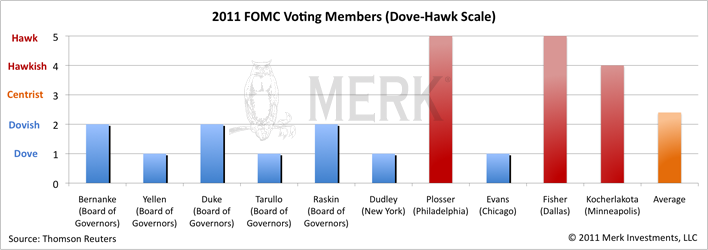

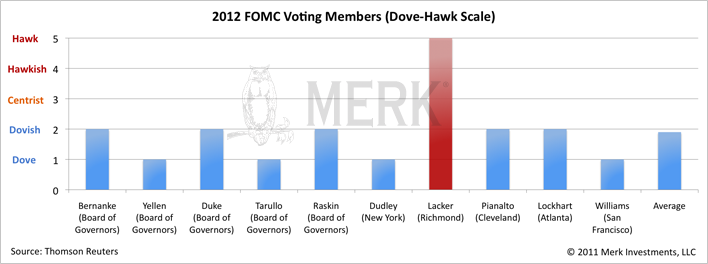

What this chart shows is that recent communication and action by the Fed may have contributed to an environment closer to where Bernanke would like to see: with inflation expectations low, Bernanke is back in familiar territory, able to print more money. A reason why the Fed first needed to set the stage is because the Federal Open Market Committee (FOMC) has a couple of outspoken hawks1 that, as we have alluded to, are not afraid to voice their dissent:  Incidentally, the 2012 FOMC composition reflects that hawks are snowbirds; only one hawk will remain. A stranded hawk may be noisy (dissent and speak out), but might stand little chance against a flight of doves2:  Let us review the Bernanke playbook; all quotes below are taken from his 2002 speech: Bernanke is determined

|

|

|

|

10-04-2011, 11:54 PM

|

#3 |

|

|

Enough said. While the markets have been “disappointed”, when push comes to shove, Bernanke has stuck to his playbook. He has paved the way for QE3. We have argued that there may not be such a thing as a safe asset anymore, and that investors may want to take a diversified approach to something as mundane as cash. Investors may want to actively manage their U.S. dollar risk, be that for their domestic or international investments. After all, investors may want to position their portfolios to take the risk that Bernanke will do what he has said into account. We manage the Merk Hard Currency Fund, the Merk Asian Currency Fund, the Merk Absolute Return Currency Fund, as well as the Merk Currency Enhanced U.S. Equity Fund. Please join us for our Quarter 3 Merk Webinar on Thursday, October, 20th at 4:00pm ET / 1:00pm PT. To learn more about the Funds, please visit www.merkfunds.com. Please sign up to our newsletter to stay in the loop as this discussion evolves. Axel Merk Manager of the Merk Hard, Asian and Absolute Currency Funds, www.merkfunds.com Axel Merk, President & CIO of Merk Investments, LLC, is an expert on hard money, macro trends and international investing. He is considered an authority on currencies. The Merk Hard Currency Fund (MERKX) seeks to profit from a rise in hard currencies versus the U.S. dollar. Hard currencies are currencies backed by sound monetary policy; sound monetary policy focuses on price stability. The Merk Asian Currency Fund (MEAFX) seeks to profit from a rise in Asian currencies versus the U.S. dollar. The Fund typically invests in a basket of Asian currencies that may include, but are not limited to, the currencies of China, Hong Kong, Japan, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan and Thailand. The Merk Absolute Return Currency Fund (MABFX) seeks to generate positive absolute returns by investing in currencies. The Fund is a pure-play on currencies, aiming to profit regardless of the direction of the U.S. dollar or traditional asset classes. The Merk Currency Enhanced U.S. Equity Fund (MUSFX) seeks to generate total returns that exceed that of the S&P 500 Index. By employing a currency overlay, the Merk Currency Enhanced U.S. Equity Fund actively manages U.S. dollar and other currency risk while concurrently providing investment exposure to the S&P 500. The Funds may be appropriate for you if you are pursuing a long-term goal with a currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Funds and to download a prospectus, please visit www.merkfunds.com. Investors should consider the investment objectives, risks and charges and expenses of the Merk Funds carefully before investing. This and other information is in the prospectus, a copy of which may be obtained by visiting the Funds' website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest. Since the Funds primarily invest in foreign currencies, changes in currency exchange rates affect the value of what the Funds own and the price of the Funds' shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, emerging market risk, and relatively illiquid markets. The Funds are subject to interest rate risk, which is the risk that debt securities in the Funds' portfolio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities, such as for- ward contracts, which can be volatile and involve various types and degrees of risk. If the U.S. dollar fluctuates in value against currencies the Funds are exposed to, your investment may also fluctuate in value. The Merk Currency Enhanced U.S. Equity Fund may invest in exchange traded funds ("ETFs"). Like stocks, ETFs are subject to fluctuations in market value, may trade at prices above or below net asset value and are subject to direct, as well as indirect fees and expenses. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. For a more complete discussion of these and other Fund risks please refer to the Funds' prospectuses. This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice. Foreside Fund Services, LLC, distributor. 1Generally speaking, a central banker may be considered a hawk if his or her monetary policy stance is perceived to focus more on inflation and less on expansionary policies. 2Generally speaking, a central banker may be considered a dove if his or her monetary policy stance is perceived to focus more on stimulating employment and economic growth and less on inflation. HOW TO INVEST Download Prospectus MERK INSIGHTS UPCOMING EVENTS Merk Quarter 3 Webinar 10/20 at 4:00pm ET / 1:00pm PT Click to Register Merk Currency Enhanced U.S. Equity Fund Introduction Webinar Click for Replay MERK IN THE NEWS Watch Coverage Bloomberg TV Sep 9, 2011 Watch Coverage More media appearances... > SUSTAINABLE WEALTH AXEL MERK WROTE THE BOOK ON SUSTAINABLE WEALTH Learn More or Order Today!  Before investing you should carefully consider the Fund's investment objectives, risks, charges and expenses. This and other information is in the prospectus, a copy of which may be obtained by clicking here. Please read the prospectus carefully. Foreside Fund Services, LLC, distributor. |

|

|

| Reply to Thread New Thread |

«

Previous Thread

|

Next Thread

»

Linear Mode

Linear Mode

| Currently Active Users Viewing This Thread: 1 (0 members and 1 guests) | |

|

|